Oregon law mandates that all drivers carry valid auto insurance before operating a vehicle on public roads. This ensures that any damages or injuries resulting from an accident are covered, protecting both motorists and the public. Car insurance requirements in Oregon are enforced under ORS Chapter 806, and compliance is verified through the DMV’s insurance reporting system. Driving without required coverage can lead to fines, license suspension, vehicle registration holds, and additional reinstatement fees. Liability coverage, in particular, guarantees compensation for bodily injury and property damage, creating a legal and financial safety net for everyone on the road.

Every Oregon vehicle owner must maintain at least the state-required minimum insurance coverage and carry valid proof of insurance whenever operating a vehicle with an Oregon License Plate. These liability insurance requirements apply to all vehicles registered under an Oregon License Plate, including during initial registration, renewal periods, and https://www.oregon.gov/odot/dmv/Pages/index.aspx residency changes, ensuring continuous coverage as required by state law. The Oregon DMV monitors compliance through the Automobile Insurance Verification Program, which requires insurers to report active policies. This page provides clear guidance on required coverage limits, acceptable documentation, insurance verification procedures, penalties for lapses, and exemptions for certain vehicles, helping drivers maintain uninterrupted registration, avoid legal issues, and meet financial responsibility requirements on Oregon roadways.

Why Oregon Requires Auto Insurance

Oregon requires all drivers to carry auto insurance to protect both themselves and others on the road. This ensures that anyone injured or whose property is damaged in a car accident has access to financial compensation. The primary reason Oregon enforces https://oregon.public.law/statutes/ors_chapter_806 auto insurance is public safety. Without liability coverage, drivers might not be able to pay for injuries or property damage after an accident, leaving victims without support. By requiring insurance, the state reduces financial risk for everyone on its roads.

Oregon law also establishes a financial responsibility system. This law obligates drivers to prove they can cover costs related to accidents they cause. Maintaining state-mandated liability coverage is one way to meet this requirement. Drivers can show proof https://dfr.oregon.gov/Pages/index.aspx through an insurance policy, a certificate of self-insurance, or other legally accepted forms. The Oregon Department of Transportation (DMV) and the Division of Financial Regulation enforce these rules. They monitor insurance compliance through regular verification programs and vehicle registration checks. Drivers who fail to maintain coverage may face penalties, including fines, license suspension, or registration holds.

Key benefits of mandatory insurance in Oregon include:

- Protection for drivers, passengers, and pedestrians

- Coverage for property damage to vehicles and other structures

- Financial support for medical expenses after accidents

- Compliance with state liability coverage mandates

This system ensures that all Oregon drivers share responsibility for road safety and financial accountability. It also helps maintain lower costs for insurance and claims statewide by reducing unpaid claims. By requiring insurance, Oregon balances individual responsibility with public protection, making roads safer for everyone.

Minimum Insurance Coverage Required in Oregon

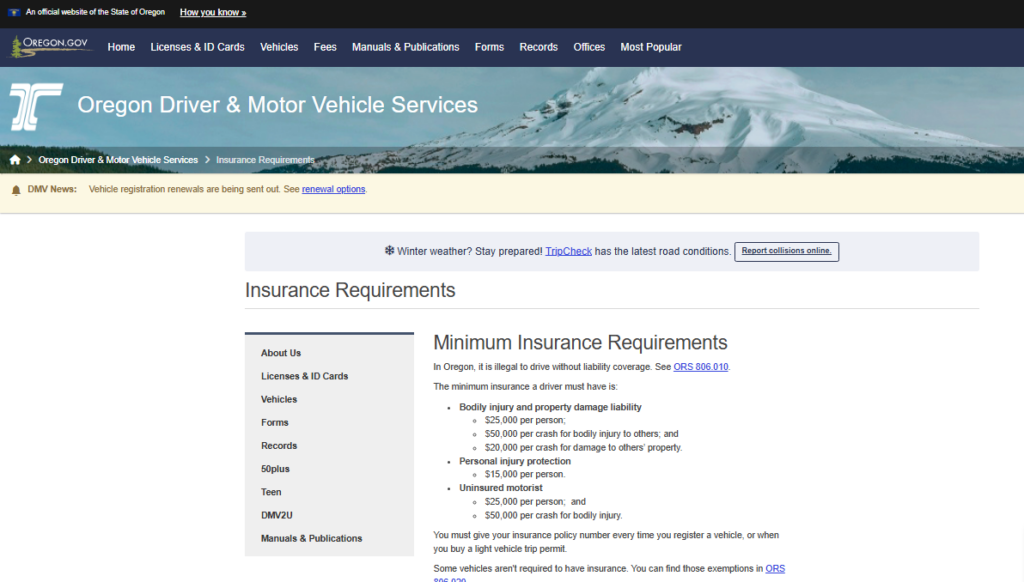

Oregon requires all drivers to carry a minimum level of auto insurance to legally operate a vehicle. This ensures that drivers can cover damages and medical expenses if they are involved in an accident. The specific coverage requirements are essential for https://oregon.public.law/statutes/ors_806.070 complying with state law and protecting yourself financially. Oregon sets clear minimums for liability, personal injury protection, and uninsured or underinsured motorist coverage. Each type of insurance serves a distinct purpose and ensures that drivers are responsible for damages or injuries they may cause.

Mandatory Liability Coverage

Liability coverage is the core of Oregon’s minimum insurance requirements. It protects https://www.oregon.gov/odot/DMV/pages/driverid/insurance.aspx other drivers, passengers, and property in accidents caused by the policyholder.

Oregon’s minimum liability coverage includes:

| Coverage Type | Minimum Amount | Explanation |

|---|---|---|

| Bodily injury per person | $25,000 | Pays for injury or death of one person in an accident caused by the insured driver |

| Bodily injury per accident | $50,000 | Total coverage for all injuries or deaths in a single accident |

| Property damage per accident | $20,000 | Pays for damage to another person’s property, such as vehicles or structures |

This coverage is commonly referred to as “25/50/20, shorthand for the three minimum amounts listed above. For example, a driver with this policy can cover up to $25,000 for one person’s injuries, $50,000 for multiple injuries, and $20,000 for property damage in a single accident. Liability insurance does not cover the policyholder’s own medical bills or vehicle repairs.

Personal Injury Protection

Personal Injury Protection (PIP) covers medical expenses and certain lost wages for the policyholder and passengers after a car accident, regardless of who caused it. Oregon requires a minimum of $15,000 per person for PIP.

PIP can cover:

- Hospital and doctor visits

- Rehabilitation and therapy costs

- Lost income due to injury

- Funeral expenses in severe cases

Having PIP ensures that drivers and passengers have immediate financial support after an accident. It is separate from liability insurance and is designed to reduce financial strain from injuries.

Uninsured/Underinsured Motorist Coverage

Oregon also requires uninsured or underinsured motorist coverage. This protects drivers if they are hit by someone who either has no insurance or insufficient coverage. Minimum coverage amounts match liability limits: $25,000 per person, $50,000 per accident, and $20,000 property damage.

UM/UIM coverage helps pay for:

- Medical bills caused by an uninsured driver

- Vehicle repair costs if the at-fault driver cannot pay

- Legal expenses if necessary

By including UM/UIM, drivers are shielded from financial loss caused by others’ failure to maintain insurance. This coverage ensures that even in worst-case scenarios, drivers are not left responsible for high medical or property costs.

Proof of Insurance: What Counts in Oregon

In Oregon, drivers must carry proof of insurance whenever they operate a motor vehicle. The state accepts several formats to verify that coverage meets minimum legal requirements. Oregon law, outlined in ORS 806.010 and related Oregon Administrative Rules (OAR), https://www.oregon.gov/odot/dmv/pages/driverid/insurance.aspx, mandates that vehicle owners maintain financial responsibility at all times. This includes presenting acceptable proof of insurance during registration, inspections, or if a law enforcement officer requests it. Failure to provide proof can result in fines, suspension of driving privileges, and registration holds.

Acceptable Proof of Insurance

The state recognizes multiple forms of documentation as valid proof. Drivers should ensure their documents clearly indicate coverage for the registered vehicle and meet the Oregon minimum liability limits.

Acceptable formats include:

- Insurance Identification Card: Both paper and electronic versions issued by a licensed insurance company are valid. The card should show the policy number, coverage dates, and vehicle information.

- Insurance Policy or Binder: A current insurance policy or temporary binder issued by the insurer can serve as proof, particularly for new or recently purchased vehicles.

- Letter from Insurance Agent: Written confirmation from an authorized agent, detailing coverage and policy details, is acceptable for short-term proof or during registration.

- Certificate of Self-Insurance: Registered self-insured drivers receive a certificate from the Oregon DMV, which counts as official proof for all compliance checks.

DMV Insurance Verification

The Oregon DMV Insurance Verification Program cross-checks registration records to ensure all vehicles remain continuously insured. Insurance companies report active policies directly to the DMV, reducing the need for repeated document submission. Still, drivers should carry physical or electronic proof while driving to avoid penalties during traffic stops or audits.

Key points for vehicle owners:

| Document Type | Notes |

|---|---|

| Insurance ID Card | Paper or electronic, must include policy number and coverage dates |

| Policy or Binder | Useful for new registrations or recent coverage changes |

| Agent Letter | Short-term confirmation, must detail coverage and vehicle info |

| Self-Insurance Certificate | Issued by DMV for qualified self-insured drivers |

Maintaining valid proof of insurance protects drivers from fines and ensures smooth registration and verification. Every form must clearly reflect coverage that meets Oregon’s minimum liability requirements, including bodily injury, property damage, and personal injury protection.

How the DMV Verifies Insurance Coverage

The Oregon DMV actively verifies that all registered vehicles have valid insurance. This process ensures drivers meet state minimum coverage requirements and maintain continuous protection while on the road. The DMV insurance verification system checks vehicle insurance through monthly and random reports from insurance companies. Every licensed insurer operating in Oregon is required to submit timely insurance reporting to DMV, including policy numbers, effective dates, and vehicle identification numbers (VINs). This helps the DMV confirm that each vehicle is covered according to state law and identifies any lapses in coverage.

Monthly and Random Verification Process

Oregon insurance companies report active policies to the DMV every month. Additionally, the DMV may conduct random verifications to ensure compliance. These checks compare DMV records with the insurance database, identifying discrepancies such as expired policies, cancelled coverage, or mismatched VINs. If a vehicle is found without valid coverage, the DMV sends a Notice of Insurance Cancellation to the registered owner. The notice gives the vehicle owner 45 days to provide proof of insurance. During this period, registration and driving privileges may be temporarily flagged until proper coverage is verified.

Consequences of Non-Compliance or False Reporting

Failing to respond to DMV inquiries or providing false insurance information can lead to serious consequences. This includes:

- Suspension of vehicle registration

- Suspension of driving privileges

- Requirement to file an SR‑22 certificate confirming financial responsibility

- Payment of a $75 reinstatement fee

Insurance agencies also face penalties if they fail to report accurate coverage information. The system relies on timely, precise insurance reporting to the DMV to protect both drivers and the public.

How Insurance Agencies Report to the DMV

Agencies submit reports electronically using standardized DMV forms. These reports include:

| Required Information | Purpose |

|---|---|

| Policy Number | Matches coverage to vehicle and owner |

| VIN | Confirms which vehicle is insured |

| Coverage Effective Dates | Ensures continuous protection |

| Cancellation or Lapse Notices | Alerts DMV of gaps in coverage |

This reporting ensures that every vehicle in Oregon has verified, minimum liability coverage, and allows the DMV to act quickly if insurance lapses occur.

Insurance & Vehicle Registration Rules

All vehicles in Oregon must have valid insurance before registration or renewal. New residents are required to obtain Oregon-compliant coverage within 30 days of establishing residency, and continuous coverage is necessary to keep registration active. Oregon law requires every vehicle owner to provide proof of liability insurance when registering a car. The Oregon DMV registration insurance process ensures that all vehicles meet state minimum coverage standards before they are legally allowed on the road. Vehicle owners can submit insurance information in person, online, or by mail when renewing or registering a vehicle. Without verified insurance, the DMV will not issue or renew registration.

New Resident Insurance Obligations

Drivers who move to Oregon must comply with local insurance rules within 30 days of establishing residency. This includes obtaining liability coverage that meets state minimums and providing documentation to the DMV. Vehicles brought from another state cannot be registered in Oregon unless proof of valid Oregon-compliant insurance is provided.

Key points for new residents:

- Provide proof of insurance meeting Oregon’s minimum liability coverage

- Include the vehicle identification number (VIN) on all documents

- Submit insurance documents before attempting registration or renewal

Continuous Coverage Requirement

Oregon requires continuous insurance coverage on all registered vehicles. If coverage lapses, the DMV may suspend registration until valid insurance is confirmed. Vehicle owners are notified if their insurance is canceled or expires, and they must provide updated proof to avoid penalties.

Continuous coverage ensures:

- Driving privileges remain active

- Vehicle registration stays valid

- Compliance with Oregon vehicle insurance rules

Vehicle owners can maintain coverage through monthly payments or policy renewals. Many insurers offer automatic renewal notifications to help prevent lapses. Maintaining uninterrupted coverage protects drivers from fines, registration suspension, and additional fees.

Penalties for Driving Without Required Insurance

Driving without the required insurance in Oregon can lead to serious consequences, including fines, license suspension, and vehicle registration issues. Vehicle owners who fail to maintain coverage may also need to file an SR‑22 to restore driving privileges. Oregon law treats https://www.oregon.gov/odot/dmv/pages/driverid/sr22.aspx uninsured driving as a significant offense. A Class B traffic violation may be issued to drivers who operate a vehicle without proof of liability coverage. The fines for such violations can reach $1,000, depending on the circumstances and prior offenses. Beyond monetary penalties, the Oregon DMV may suspend a driver’s license for up to one year until valid insurance coverage is confirmed.

Registration Suspension

Vehicle registration is closely tied to active insurance coverage. If insurance lapses, the DMV can suspend vehicle registration, preventing legal operation on public roads. Vehicle owners receive a Notice of Insurance Cancellation, and they have 45 days to provide proof of coverage. Failing to comply within this period may result in both registration and driving privileges being suspended simultaneously.

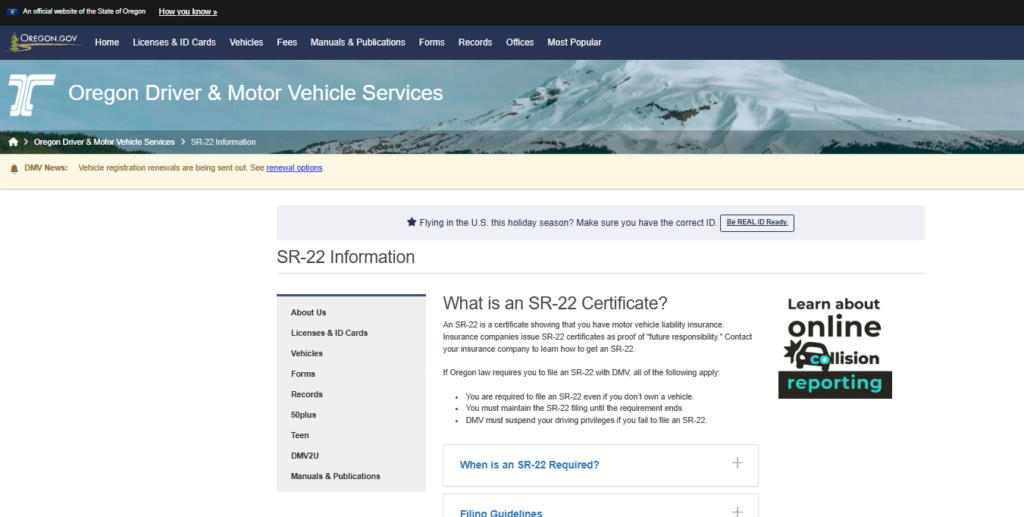

SR‑22 Requirements

An SR‑22 certificate is a form filed by an insurance company with the DMV to verify that a driver carries the required liability coverage. Drivers who have experienced lapses in coverage or serious violations must maintain an SR‑22, typically for three years, to regain full driving privileges. SR‑22 filing demonstrates continuous financial responsibility and is often required after insurance cancellations, accidents, or repeat offenses.

Exceptions & When Insurance Isn’t Required

In Oregon, certain vehicles are legally exempt from carrying auto insurance. These exceptions allow specific types of vehicles to operate without liability coverage under state law, as outlined in ORS 806.020.

Oregon law recognizes that not all vehicles pose the same risk on public roads. Vehicles owned by the government, farms, or tribal entities may operate without standard insurance requirements. For example:

- Government vehicles: Cars, trucks, or other motor vehicles owned by the United States, the state of Oregon, or any local government.

- Tribal vehicles: Vehicles operated within federally recognized Indian reservations.

- Farm equipment and implements of husbandry: Tractors and farm machinery occasionally driven on public highways.

- Dealer vehicles: Licensed motor vehicle dealers may use dealer plates without individual vehicle insurance, provided the dealer maintains a garage liability policy.

- Self-insured vehicles: Those certified as self-insured by the Oregon Driver and Motor Vehicle Services Division.

Insurance coverage is generally not required for vehicles that do not operate on public roads. This includes off-road vehicles, all-terrain vehicles, and antique vehicles used strictly on private property. Owners must ensure that the vehicle remains off public roadways to maintain the exemption.

Optional & Recommended Coverage Beyond Minimums

Oregon drivers can choose coverage that goes beyond the state’s minimum requirements to protect their vehicles and finances. Collision, comprehensive, and higher liability coverage provide extra financial protection that can prevent costly out-of-pocket expenses after an accident.

Collision and Comprehensive Coverage

Collision insurance covers damage to a driver’s vehicle resulting from an accident, regardless of who is at fault. Comprehensive coverage protects against non-collision events such as theft, vandalism, fire, or severe weather damage. Together, these policies form what many insurers call full coverage, which is often required by lenders when a vehicle is financed or leased.

- Collision: Repairs or replacement of your vehicle after a crash.

- Comprehensive: Protection from natural disasters, theft, or vandalism.

- Full Coverage: Combines collision and comprehensive with required liability limits.

Having collision and comprehensive coverage can prevent drivers from paying thousands of dollars for vehicle repairs, particularly for newer or high-value cars. According to the Oregon Division of Financial Regulation, vehicles with a market value over $10,000 benefit most from full coverage to avoid financial strain after accidents or damage.

Higher Liability Coverage

Oregon law sets minimum liability coverage at $25,000 per person and $50,000 per accident for bodily injury, with $20,000 for property damage. Many drivers purchase higher liability coverage to protect personal assets if they cause serious injury or extensive property damage.

- Why it matters: Minimum coverage may not cover medical bills or vehicle replacement costs in major accidents.

- Recommended limits: $100,000/$300,000 bodily injury and $50,000 property damage are common.

Full Coverage Recommendations

Drivers who want maximum protection often combine full coverage with higher liability limits. This combination provides:

- Complete financial protection for the driver and passengers.

- Peace of mind during high-risk situations such as accidents, storms, or theft.

- Compliance with lender requirements for financed vehicles.

Investing in optional coverage safeguards both the vehicle and the driver’s finances, making it a smart decision for anyone who wants strong financial protection on Oregon roads.

FAQ About Car Insurance Requirements

Many drivers have questions about Oregon’s car insurance requirements, especially when it comes to registration, driving someone else’s car, or dealing with policy lapses. This FAQ answers the most common concerns and explains what vehicle owners need to know about proof of insurance, minimum coverage, and DMV verification.

Do I Need Insurance to Title a Car?

Yes, Oregon requires valid insurance before a vehicle can be titled. Vehicle owners must show proof that their car meets the state’s minimum coverage requirements for liability. This includes coverage for bodily injury and property damage. The DMV will not process a title without an active policy, and the proof must clearly list the vehicle identification number (VIN), policy number, and effective coverage dates. Ensuring insurance is active at the time of registration prevents delays and keeps drivers compliant with DMV verification requirements.

Can I Drive Someone Else’s Car?

Driving another person’s car is allowed only if you are covered under their policy or the insurance includes permissive use. Oregon law requires that all vehicles on public roads carry valid liability insurance, regardless of who is driving. Checking with the vehicle owner and their insurance provider is essential, as some policies automatically extend coverage to occasional drivers while others do not. Without confirmation, you could be personally responsible for damages or injuries, and the DMV may consider the vehicle uninsured during verification.

What to Do if My Insurance Is Canceled?

If an insurance policy is canceled, the vehicle owner must obtain new coverage immediately. Driving without insurance is a violation of Oregon law and can lead to fines, suspension of driving privileges, and SR‑22 filing requirements. The DMV typically issues a Notice of Insurance Cancellation, giving drivers 45 days to provide proof of continuous coverage. Once a new policy is secured, it should be submitted to the DMV to reinstate registration and maintain compliance. Continuous coverage prevents legal penalties and additional fees associated with insurance lapses.

Does Oregon Require No‑Fault Insurance?

Oregon does not require no-fault insurance. Drivers are legally obligated to maintain liability coverage for bodily injury and property damage, and accidents are handled under a traditional fault-based system. While optional coverages like collision, comprehensive, and personal injury protection (PIP) can supplement liability insurance, they are not mandatory unless a lender requires them. Maintaining the state minimum coverage ensures both compliance with the law and financial protection in the event of an accident.

What Happens if I Drive Without Insurance in Oregon?

Driving without insurance in Oregon is considered a serious violation of state law. Vehicle owners must maintain at least the minimum coverage for liability at all times, and failure to do so can result in fines, suspension of driving privileges, and vehicle registration holds. The DMV monitors insurance compliance through its verification system, and drivers may receive a notice to provide proof of coverage within a specified period. In some cases, an SR‑22 certificate is required to reinstate driving privileges, which demonstrates financial responsibility to the state. Maintaining continuous insurance not only avoids these penalties but also ensures protection against accidents, injuries, and property damage while driving.